.png)

Cars, Vans and Mileage Allowances

- UPECO Columnist

- May 24

- 4 min read

For many small companies in England and across the UK, vehicles are part of everyday business. A director may use their own car for client visits. A company may provide a van to an employee. A business may also consider buying or leasing a company car.

From 6 April 2026, some important tax figures changed. These changes are not difficult to understand, but they are worth checking before a company provides a vehicle or pays mileage.

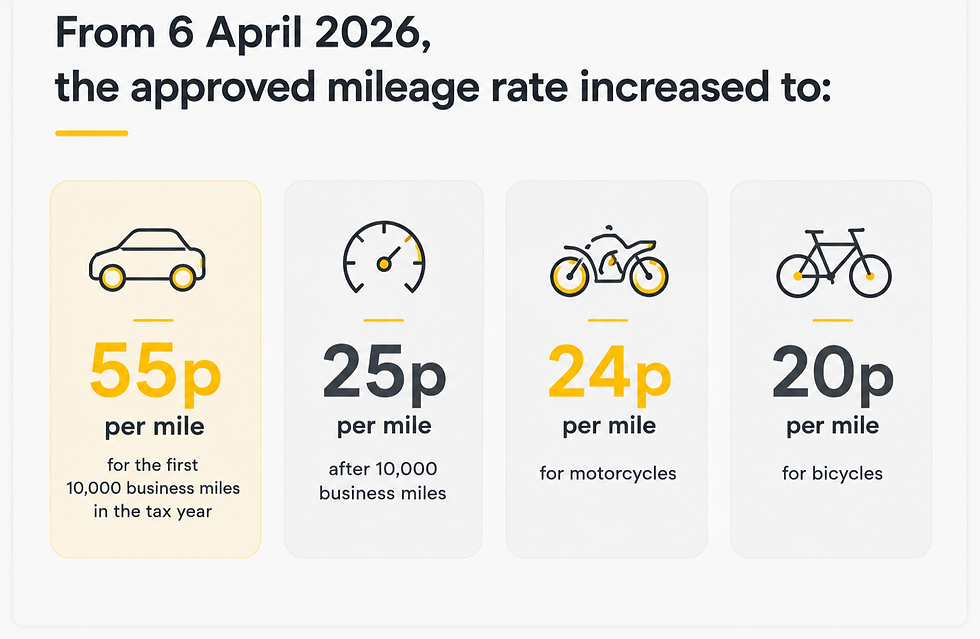

Quick summary

The approved mileage rate for cars and vans increased to 55p per mile for the first 10,000 business miles.

The taxable benefit for company vans increased to £4,170.

The car fuel benefit multiplier increased to £29,200.

The van fuel benefit increased to £798.

Company car tax still depends mainly on the car’s list price, emissions, fuel type and private use.

1. Company cars

A company car can be useful, but it can also create a tax charge for the director or employee if there is private use.

For 2026/27, HMRC added the updated company car percentages. A zero-emission company car is generally taxed at 4% of the relevant car value. Higher-emission cars can be taxed at much higher percentages, up to 37%.

This means that electric and low-emission cars can still be more tax-efficient than many petrol or diesel cars. However, the tax cost should always be checked before the company agrees to buy, lease or provide the car.

2. Company fuel

Company fuel is often more expensive from a tax point of view than people expect.

If a company pays for private fuel, there may be a separate fuel benefit charge. This applies even if the private fuel cost is not very high.

For 2026/27, the car fuel benefit multiplier increased to £29,200.

This does not mean the employee pays £29,200. It means HMRC uses this figure as part of the benefit calculation. The actual tax depends on the car’s benefit percentage and the person’s tax rate.

In practice, private fuel paid by the company is often not worth it unless the private mileage is high. For many directors, it may be cleaner to keep private fuel separate and only claim real business mileage.

3. Company vans

Company vans are common in construction, property maintenance, delivery work, cleaning, trades and service businesses.

A van can create a taxable benefit if it is available for private use. From 6 April 2026, the van benefit charge increased to £4,170.

This is a fixed figure used for the tax calculation. The actual tax paid by the employee or director depends on their personal tax rate.

There is normally no van benefit if private use is limited to very small and incidental use. However, the company should be careful. Regular personal use can create a taxable benefit.

Good records are important, especially where the van is taken home.

4. Van fuel

If the company also provides fuel for private use in a van, there may be a separate van fuel benefit.

For 2026/27, the van fuel benefit charge increased to £798.

Again, this is not the exact tax payable. It is the figure used in the benefit calculation.

If the van is only used for business, the company should keep clear records to support that position.

5. Mileage allowance

The mileage allowance change is one of the most practical updates for small companies.

This matters where a director or employee uses their own vehicle for business journeys.

For example, if a director uses their personal car to visit a client, the company can usually reimburse business mileage using the approved mileage rate. If the company pays within the approved rate, it is normally simple for payroll and tax purposes.

For many small companies, mileage claims are still the simplest option. But for electric vehicles, a company car may still be worth reviewing.

7. Practical checklist for directors

Before choosing a vehicle arrangement, ask:

Will the vehicle be owned or leased by the company?

Will there be private use?

Will the company pay for private fuel?

Is the car electric, hybrid, petrol or diesel?

What is the official list price?

What are the emissions?

Will the director use their own car instead?

Will mileage records be kept properly?

The important point is not only whether the company can pay for the vehicle. The real question is whether the tax result is sensible.

Conclusion

The 2026/27 changes make vehicle planning more important for directors and small companies.

The higher mileage rate is good news for those using their own cars for business. At the same time, company vans, fuel benefits and company cars still need careful review.

Before buying, leasing or reimbursing vehicle costs, companies should check the tax position first. A simple review can prevent unexpected benefit charges later.

© 2026 UPECO LTD

_

ATTENTION!

This article intends to give only a general informative picture and should not, in any case, be taken as a rule. It is strongly recommended to seek a full and professional guidance specifically for your circumstances before making any decisions.

Comments